overview

There was an accelerated shift towards professional service companies (comprised of engineers, accountants, pharmacists, architects, and medical and health related professionals, etc.) adopting a corporate or hybrid structure (Alternative structure) instead of the more traditional partnership of natural persons. This shift has created an area where the ATO is focused on regulatory compliance and taxpayers need to have a clear understanding of what constitutes a legitimate distribution of profits within an alternate structure, as opposed to practices that may be inappropriately taxed .

context

Professionals participating in an alternative structure are typically entitled to two types of income distributions for a relevant period of time:

- an amount representing the value of the personal services rendered to the company's customers (compensation); and

- a distribution that represents a portion of the value generated by the company's business structure, proportional to its participation in the alternative structure (Distribution of profits).

The ATO intends to enter into arrangements that can alter a professional's tax liability by diverting the income to an affiliate if that income is more thematically related to personal services (but for technical reasons, partnership income does not necessarily include a portion personal service income) – that is, increasing the distribution of profits and underestimating remuneration.

Compliance approach

While the ATO retains all of its compliance powers in relation to this issue (including Part IVA of the Income Tax Assessment Act 1936 (Cth)) (ITAA 1936)) It seems clear that the professional's obligation to self-assess is an integral part of their overall strategy to achieve full compliance.

The ATO has published the draft guideline for practical compliance with PCG 2021 / D2 (Draft Directive) to facilitate self-assessment. The draft policy contains the details of the system, which includes two "gateway" tests that must be passed in order for the taxpayer to proceed to the next step, which is self-assessment using a more detailed risk assessment matrix (if the gateway) Taxpayers must contact the ATO). The aggregated result of the self-assessment then draws a low, medium or high risk. Low risk levels attract the standard ATO compliance treatment. Medium and high risk agreements require active collaboration with the ATO.

Employed partners, whose remuneration consisted partly of a distribution to an affiliate in the past, are not covered by the draft directive and can no longer use the safe havens defined in the 2015 version of the guidelines (which have been replaced by the draft directive). Any person or company involved in such an agreement must now judge their circumstances based on the case law from Part IVA of ITAA 1936.

Gateway tests

The gateway tests are designed to capture high-risk agreements and prevent them from continuing in the self-assessment process.

Gateway 1: The arrangement must be operated commercially

There must be an economic rationale for the agreement that is documented, assessable and consistent with the economic and structural realities of the company's business. For example, a commercial justification for "protecting assets" must make a substantial improvement in these variables. Other factors to consider are:

- The arrangement is no more complex than it needs to be.

- Improved tax results are not the only benefit of the deal. and

- The agreement is permissible and falls within the scope of the relevant founding documents (e.g. constitution, partnership agreement, internal guidelines, etc.).

Gateway 2: No high-risk functions

The following agreements have high risk characteristics:

- Financing agreements in connection with transactions on market terms;

- Exploiting the difference between accounting standards and tax law;

- Arrangements in which a partner assigns a portion of a company's interest in a manner materially different from the High Court's decision in Federal Commissioner of Taxation v Everett (1980) HCA 6 (which allows for the permissible assignment of a company's interest to a related party Person included when the income was assumed to come from the business structure and not from personal services. And

- multiple classes of stocks and shares held by non-shareholders.

The taxpayer must also consider any published tax warnings listing additional agreements that are considered to be risky.

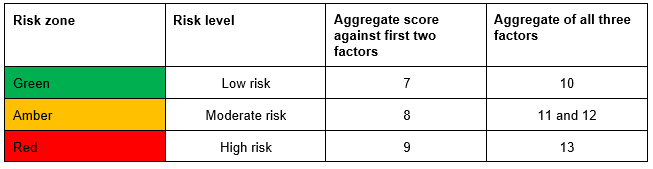

Risk assessment

The risk assessment matrix and the method of assigning the level of risk (as set out in the draft directive) are given below. In essence, the more profit is allocated to the individual professional, the lower the risk and the higher the collective effective tax rate of the individual professional and its affiliates. However, the 50% compensation allocation and 30% effective "safe havens" tax rate that existed under previous guidelines would generate a risk score of 9, which would result in at least a moderate level of risk (although 51% compensation allocation and 31% effective tax rate may be lead to a low risk).

matrix

Risk level

Next Steps

- The draft directive is not yet in final form (comments will close on March 26, 2021) but will most likely be adopted with minimal material changes.

- Companies usually have to distribute profits in such a way that the individual professional receives at least 51% of the remuneration, which corresponds to an effective tax rate of 31% or more for the professional and his affiliated companies.

- For proper compliance, it is important that all professional service companies take the following steps:

- apply a tax planning lens to any profit distribution made for the current fiscal year;

- from July 1, 2021 (or July 1, 2023 if they qualify for the transitional provisions, i.e. commercially driven agreements with no high-risk features that were entered into before December 14, 2017):

- carry out a risk assessment for profit sharing in accordance with the final version of the draft directive;

- document – and gather supporting material to demonstrate the conclusions of the risk assessment; and

- Implementation of an annual process to review the risk assessment.

- Specifically, companies should consider whether a more comprehensive tax compliance review is required with respect to profit-sharing practices (e.g. failure to record capital gains, avoidance of Division 7A of Part III of ITAA 1936, income injection for companies with excessive losses, etc.) if the intention is to contact the ATO directly for a medium or high risk agreement.

Further information

ATO draft of the guideline for practical compliance with PCG 2021 / D2 (see: PCG 2021 / D2 | Legal database (ato.gov.au))