As the 2017 tax reform law is dissected, many investors and entrepreneurs are considering the personal wealth implications around the loss of state and local tax deductions (SALT). At the root of it, tax reform limited the SALT deduction to $10,000 – which particularly impacts high-earners in high-tax states whose SALT bills typically far exceed $10,000. Which raises this consideration:

Does moving your primary residence to a tax-advantaged state make sense?

Let us help you understand some of the tax implications.

With more companies offering creative compensation packages and flexible work arrangements, you may choose to have your legal domicile in one state and work in another. As always, any solid wealth protection strategy should carefully weigh potential tax advantages with estate planning goals and quality-of-life considerations. In addition, your domicile has significant legal implications that require careful discussion with your attorney.

Whether you move or not, we explore the state tax implications of claiming a domicile vs. part-time residence, collecting equity and deferred compensation, changing family status and estate planning. As always, you should consult with a tax advisor regarding your specific situation.

How to prove domicile vs. part-time residence

You may have more than one residence but for tax purposes you only get one domicile. Your domicile state is defined as the location that you call home and the place where you always intend to return.

In the case of Dorothy in The Wizard of Oz, her domicile is Kansas and her part-time residence while out wandering about is Oz.Consulting with your tax advisor will help square away questions about your domicile.

A move involves many considerations in addition to taxes; a change of domicile likely will mean a profound shift for you and others in your life.

If taxes were the only consideration, you wouldn’t think twice about leaving California, with a state income tax rate of 13.3%, and decamping to Alaska, with no state income or estate tax and robust asset protection laws.

States generally use a “six-month presumption”, declaring that living in a state for six months (183 days) per year qualifies you as a domiciled resident. However, simply residing outside a high-tax state for 183 days per year is not enough to gain a tax advantage. There are other domiciled residency criteria, which if unsatisfied, could jeopardize your low-tax residency strategy and trigger a state tax authority “residency audit”.

For example: If a state finds you’ve made significant taxable income and have meaningful contacts (such as a second home, material business interests or visit the state for extended periods), you could face a “residency audit”.

Failure to meet state residency requirements may negate the tax benefits you hope to achieve and result in orders to pay back taxes with penalties.

How state income taxes are applied

State income tax filings may consist of: (1) the primary state tax by your domiciled state, (2) any secondary income tax for any part-time residency state and filing with that respective part-time state, (3) credits your domiciled state will give for the payment of the secondary tax. Primary residents are taxed by their domicile state (unless the state has no income tax) on ALL income, including income from sources outside of their domicile state. Generally, when living for a period and earning income in another state, that state taxes only what was earned during the part-time residency. However, some domicile states will give you a credit for income taxes paid on earnings made in another state.

For example: If you’re domiciled in New York, but moved for a period to Massachusetts to work for a local company there, you would pay income tax on only those earnings to Massachusetts and on all earnings to New York.

Potential implications with equity and deferred compensation

Under tax rules, even though you may participate in a deferred compensation program sourced in one state and then move to a lower-tax state, the deferred compensation would be taxed by the previous state. However, if you elect to take the deferred compensation payments over a period of more than 10 years, the tax on the deferred compensation payments is set at the rate applied by your domicile state when you receive the payments.

For example: If you participated in a deferred compensation program in Massachusetts and then made Florida, which has no income tax, your new domicile, all the deferred income you collect in Florida will be taxed by Massachusetts at its 5.1% income tax rate (unless the payments are spread over more than 10 years). If you have ISOs, NSOs or RSUs, the taxes are applied based on where the shares vested, not where they were granted.

For example: If you had 100,000 RSUs and 80,000 of them vested before you moved from California to Massachusetts, then, the 80,000 would be taxed by California. The remaining unvested RSUs would be considered earned in Massachusetts.

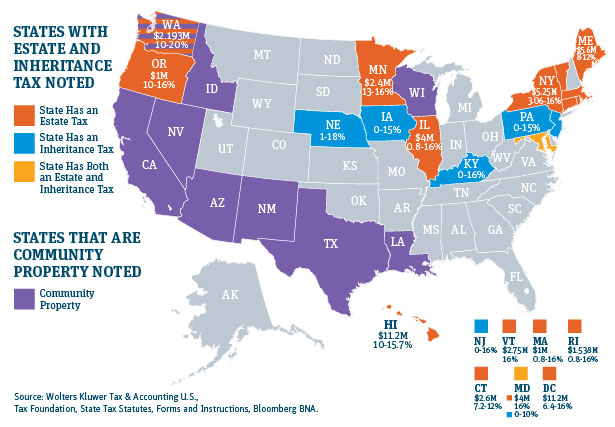

Understand how state family law varies

Community property states stipulate that marital property is owned by both spouses equally (50/50) and includes earnings, purchases made with those earnings and debts accrued during the marriage. Community property states also consider assets owned before marriage as separate property. It may seem that keeping “separate property” and “community property” straight is easy, but then consider the consequences of filing separate or joint state/federal tax returns. Or how do you account for using “community income” to pay the mortgage on one’s “separate property”? It’s tricky.

Marital assets following a divorce, legal separation or death are divvied up differently depending on whether you live in a common law property state or a community property state. If you are changing your marital status, consult a state-specific family law attorney and tax advisor.

Keep in mind that some states have specific exclusion amounts and exemption rates for estate and/or inheritance tax that differ from the federal lifetime exclusion rate. This may impact current language in an existing estate plan. State legislation may change often, and particularly now with the doubling of the individual federal lifetime exemption to $11.18 million.

Finally, depending on your situation, change of domicile may not be necessary or beneficial. Other solutions include the establishment of a trust or LLC in a more tax-advantaged state.

Plan a strategy with SVB Private at your side

Planning a tax-efficient strategy and implementing it will take time. Contact your SVB Private Relationship Manager to get started. As your primary contact, your Relationship Manager can help guide you and connect you with other professional advisors, and we recommend that you seek counsel from your tax professional and estate plan professional, to work with us and design the best wealth strategy for you.