Kelly Sullivan/Getty Images Entertainment

Thesis

After Meta Platforms (NASDAQ:FB) reported its results on April 27, its share price surged by as much as 17% during after-market trading. And as I wrote this (before the market opened on April 28), its share price is up by more than 16% (about $200). The prices might have changed a bit again when you read given the market volatility.

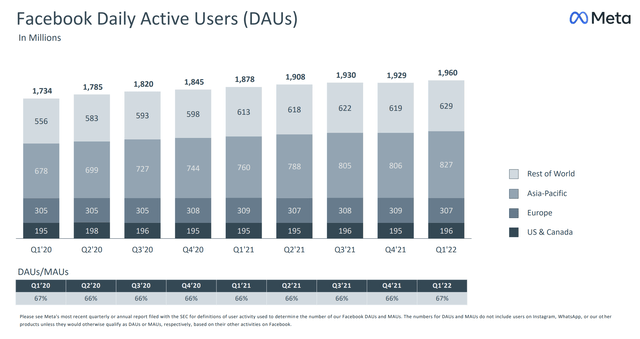

The thesis here is that even after this large price surge, its growth potential is still not properly priced. In my view, the business reported strong performance across the board, and at the same time actively invested in high-growth future areas. Firstly, the core business remains intact and strong. The key fundamental metrics, as shown in the chart below, maintain healthy growth. Daily active users (“DAUs”) continued their growth and rose 4% to 1.96 billion in Q1 2022, topping expectations there. Monthly active users rose 3% to 2.94 billion. A few more highlights as reported by Seeking Alpha news:

- The daily active users across all its family of apps (such as Facebook, Messenger, Instagram, WhatsApp) rose 6% to 2.87 billion.

- More importantly, Ad impressions delivered across the Family of Apps” (Facebook, Messenger, Instagram, WhatsApp) rose by 15% year-over-year, and the average price per ad fell by 8% in that span.

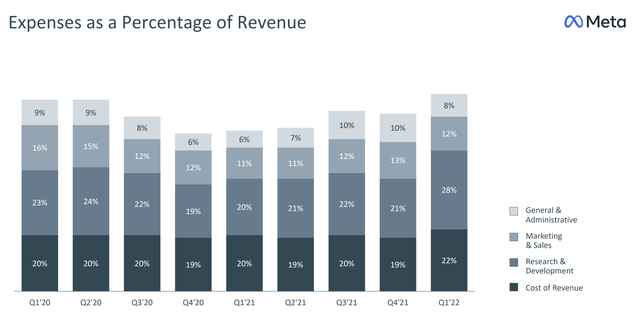

Furthermore, the business invests heavily in R&D, and its R&D expenses reached a record-setting 28% of sales in Q1 2022. The business enjoys a high yield from its R&D efforts in the past. I am optimistic that such investments will accelerate its key investment areas such as AI infrastructure, Business Platform, and Reality Labs, and will fuel its growth in the years to come.

However, such growth potential is still not fully priced in even after the large price surge. It is still a growth stock priced like a value stock according to what I call Buffett’s 10x pretax rule. As to be detailed later, it’s current priced at only about 10.9x of pre-tax earnings based on its FW 2022 earnings, effective tax rates, adjusted for its current liquidity.

FB 2022 Q1 earnings report

FB’s R&D Efforts And R&D Yield

First, I do not invest in a given tech stock because I have high confidence in a certain product that they are developing in the pipeline. Instead, I feel more comfortable betting on A) the recurring resources available to fund new R&D efforts sustainably, and B) the overall efficiency of the R&D process.

So let’s first see how well and sustainably FB can fund its new R&D efforts. FB’s R&D expenses reached a record-setting 28% of sales in Q1 2022 as shown in the chart below. To put things under perspective, FB has been spending on average 20% of sales on R&D in the past five years. And its closest competitor in the digital ad space, Google (GOOG), spends on average 15% of sales on R&D in the past 5 years. Such substantial ramp-up of R&D efforts shows me shows that A) the business is confident in its earnings consistency and growth, and B) the business has no lack of future directions to pursue (such as AI and augmented reality). As commented by CEO Mark Zuckerberg:

“Based on the strong revenue growth that we saw in 2021, we kicked off a number of multi-year projects to accelerate some of our longer term investments, especially in our AI infrastructure, Business Platform and Reality Labs.”

FB 2022 Q1 earnings report

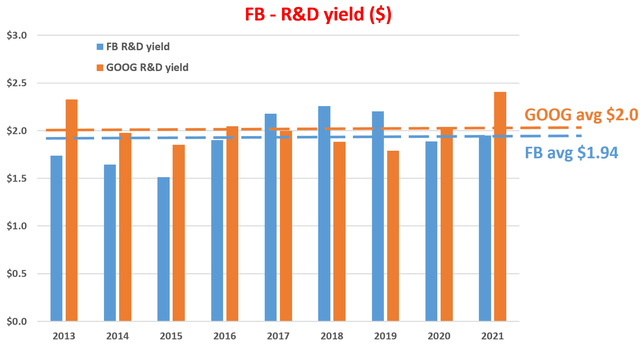

FB’s R&D process is also very effective. We ourselves like to use a variation of Buffett’s $1 test to quantify the R&D yield. We do not only listen to CEOs’ pitches on their brilliant new ideas that will shake the earth (again). We also examine the financials to see if their words are corroborated by the numbers. And in FB’s case, they are.

The following chart shows the R&D yield from FB, compared to GOOG again to set things under context. As you can see, the R&D yield for both has been remarkably consistent and has an essentially identical long-term average of $2. This level of R&D yield is very competitive even among the overachieving FAAMG group. Finally, note that as detailed in my earlier writing, the R&D yield is calculated by the following steps:

The purpose of any corporate R&D is obviously to generate profit. Therefore, it is intuitive to quantify the yield by taking the ratio between profit and R&D expenditures. This way we can quantify how many dollars of profit has been generated per dollar of R&D expenses. Here, we use the operating cash flow as the measure for profit. Also, most R&D investments typically have a lifetime of a few years and this analysis assumes a 3-year average investment cycle. And we use a 3-year moving average of operating cash flow to represent this 3-year cycle.

Author and Seeking Alpha data.

Valuation And Buffett 10x Pretax Rule

Given the above growth opportunities, consensus estimates are projecting its revenues to grow at 11.5% CAGR per year in the next five years until 2027, and its EPS to grow 10% during the same period.

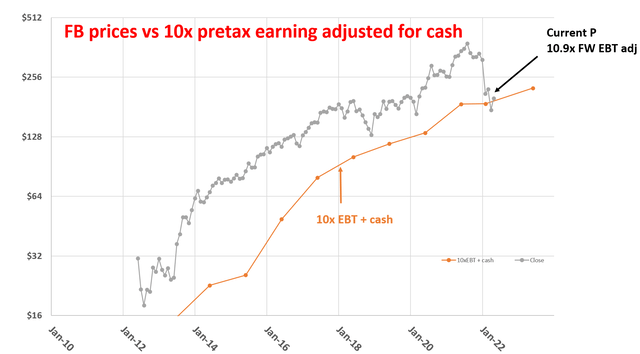

However, as you can see from the following chart, in terms of valuation, it is still priced like a value stock according to Buffett’s 10x pretext rule when adjusted for its current cash position. Its current liquidity is reported to be at $43.89 billion as of quarter-end (translating to about $16 per share), its effective tax rate is reported to be 16% from its earnings reports, and its 2022 FW EPS is estimated to be $12.16 per share. Based on these inputs, you can see that its current valuation is only about 10.9x pretax earnings after adjusting for its current cash position, really close to Buffett’s 10x pretax rule.

Author based on Seeking Alpha data

And the thesis of this chart is really simple. A stock with the quality and growth potential like FB should never trade below 10x of its pretax earnings according to what I call Buffett’s 10x pretax rule. However, at its current price, it is getting really close. As a result, the market is discounting all of its future growth potential. In case you are not familiar with the background, our earlier writings provide more details about the Buffett’s 10x pretax rule, and here is a very brief summary::

First, Buffett himself paid ~10x pretax earnings for so many of his largest and best deals, ranging from Coca-Cola, American Express, Wells Fargo, Walmart, and the more recent Apple.

Second, after-tax earnings do not reflect business fundamentals. Taxes can change from time to time due to factors that have no relevance to business fundamentals, such as tax law changes.

Third, pretax earnings are easier to benchmark against bond earnings. The best equity investments are bond-like, and when we speak of bond yield, that yield is pretax. So a 10x EBT provides a 10% pretax earnings yield, directly comparable to a 10% yield bond.

Based on the above background, if I buy a business with staying power at 10x EBT and even if the business stagnates forever, I am already making a 10% return pretax (and I would be quite happy already). Any growth is a bonus. And in FB’s case, it is very unlikely that it will stagnate. Quite the opposite, it is well poised to capitalize on strong secular growth opportunities as analyzed above given its sustainable R&D inputs, high R&D yields, strong revenues from its current digital ad business, and the potential nonlinear growth from its future areas.

A final observation about future growth before closing this article. Even though CEO Mark Zuckerberg commented below that FB is planning to “slow the pace” of some of the investments:

These investments are gonna be important for our success and growth over time, so I continue to believe that we should see them through, but with our current business growth levels, we are now planning to slow the pace of some of our investments…

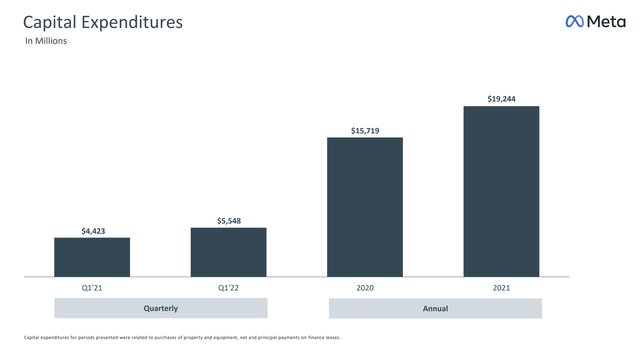

FB has been spending an increasing amount of CAPEX in recent years and reached a record $19.2B in 2021. Its CAPEX, including principal payments on finance leases, was $5.55 billion for Q1 2022. In the Q1 earnings report, its CFO commented that FB expects its 2022 capital expenditures (again including principal payments on finance leases) to be in the range of $29-34B, far exceeding the 2021 level. The increased CAPEX expenditures are another indicator of FB’s confidence and determination in its strategic areas and its growth potential.

FB 2022 Q1 earnings report

Conclusion And Risks

Despite its large price surge after reporting Q1 2022 earnings, FB is still a growth stock at a value stock price. Particularly, it’s currently priced at only about 10.9x of FW pre-tax earnings after adjusting for its current liquidity. According to Buffett’s 10x pretax rule, such a valuation also provides about 10% pretax return, comparable to a 10% yielding bond even if it stagnates forever. Yet, it has been showing healthy growth. Looking further out, FB is well-positioned with so many futuristic opportunities in augmented reality and its virtual reality business. We are also optimistic that its aggressive investing in the Metaverse division will keep generating new business ideas and growth opportunities.

Although, there are some risks involved with FB too, both at a macroscopic level and a specific level.

- First, there are considering macroscopic unfolding currently, with the Ukraine/Russian conflict and global economic slowdown as the top two. The duration and eventual outcomes of the war (as with any geopolitical conflict) are totally uncertain and could impact FB in unpredictable ways. And in the U.S., the Bureau of Economic Analysis just reported that GDP unexpectedly falls in Q1 2022 as inflation continues to rise. A recession is defined as a GDP contraction in two consecutive quarters.

- The businesses also face the possibility (although a remote one in my view) of an anti-trust regulatory risk. FB has been involved in multiple lawsuits and investigations both in the U.S. and abroad. Its investment in the metaverse is only at an incipient stage and future success is very uncertain. Management themselves acknowledges that it will be years before those efforts bear fruit. Despite FB’s heavy investment so far, the revenues in this area are currently negligible compared to its core ad business (less than $500 million in the most recent quarter).