News from US banks

Subscribe to myFT Daily Digest to be the first to know about news from US banks.

Large US banks' lending operations are doubling for wealthier customers, and wealthy Americans are borrowing to buy second homes, invest in the stock market, and potentially reduce their tax burden.

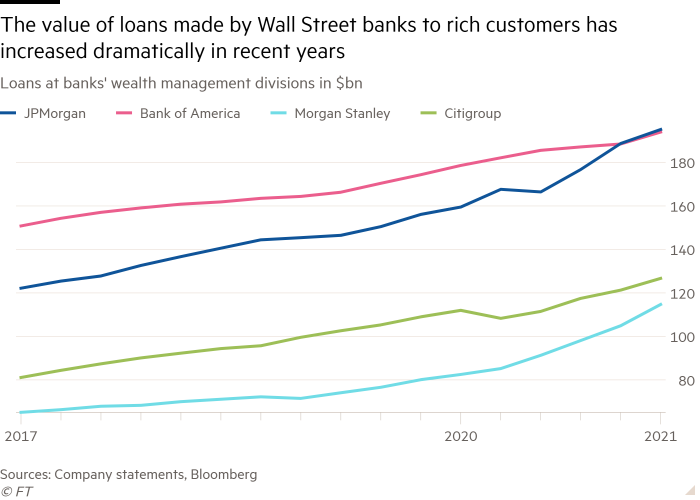

The total loan value of the asset management divisions of JPMorgan Chase, Bank of America, Citigroup and Morgan Stanley exceeded $ 600 billion in the second quarter, up 17.5 percent from a year earlier. This corresponded to 22.5 percent of the banks' total loan books compared to 16.3 percent in mid-2017.

Banks like to make these loans because they have very low losses, but they are not without risk. The market turmoil in the early stages of the Covid-19 pandemic last year prompted asset managers to ask clients to provide additional collateral.

"What worries me is that you have this flood of credit, and all of this against the background that the rich never go bad," said Peter Atwater, President of Financial Insights, citing the allowances banks keep on their asset portfolios, " poor ".

This type of borrowing has been on the rise for more than a decade, but the pace has accelerated since the Federal Reserve cut rates in response to the pandemic. For a two-year loan against liquid investments such as stocks, asset management customers can expect a rate of around 1.4 percent, according to bankers and consultants.

Recommended

"Interest rates are so remarkably low that they consider it cheap money," said Christopher Boyett, co-chair of the Private Wealth Practice at Holland & Knight law firm.

The contrast with the banks' consumer and corporate loan books is astounding. Asset management loans at JPMorgan, Bank of America, Citi and Morgan Stanley have increased 50 percent over the past four years, compared to just 9 percent of the total loan portfolio.

JPMorgan and Citi are now lending more credit to a small number of ultra-high-net-worth customers than their millions of credit card customers. A decade ago, JPMorgan loaned credit card customers five times as much as retail customers.

The Swiss bank UBS, the world's largest asset manager and a major US business, announced this week that it would be issuing more loans in the US.

The loans to high net worth borrowers are widely used for investments, as well as for the purchase of second homes and luxury goods. Investors also borrow to invest in their own businesses and bypass banks' corporate lending departments to borrow cheaper and faster.

"There has been this lifestyle change as people rethink where they want to live," said Scott Milleisen, US director of credit solutions for JPMorgan's private bank. "They need money to buy or renovate new houses and they spend money on furniture and works of art."

It is controversial that borrowing can also serve to lower taxes. Instead of selling assets to raise cash – and facing a capital gains tax bill – wealthy customers get money by borrowing against the value of their investments.

"The other way these families could get liquidity from these assets would be to sell them, which of course would have tax implications that would not be cheap," said Sabrena Silver, partner at White & Case law firm.

Silver said the tax issue is "relevant but not a priority" to wealthy customers of the banks, but critics of the practice disagree.

Frank Clemente, executive director of the liberal advocacy group Americans for Tax Fairness, said wealthy borrowers were involved in "legal tax evasion."

"The rich operate under a completely different tax system where all that accumulated wealth is not taxed unless you sell – and they're so rich they don't have to sell," said Clemente.

Emmanuel Saez and Gabriel Zucman, economists at the University of California at Berkeley, estimated earlier this year that U.S. billionaires had total assets of $ 4.25 trillion, of which $ 2.7 trillion was untaxed profits.

The tax bill proposed by the Biden government would increase taxes on capital gains from 20 percent to 39.6 percent and close the so-called “tiered base” loophole that enables wealthy families to transfer capital gains tax-free between generations.

Such an increase in capital gains tax could boost lending to the rich even further. However, advisors believe that bank asset management lending is likely to be more dependent on interest rates than Washington's fiscal policy.

"I don't see it as tax-motivated as it is investment-motivated," Boyett said. "The appeal will fade when prices go up."